Budget day update, 30 October 2024

The budget has been published, and there were no changes to the income tax position of pensions. This is to be welcomed, consumers need to have certainty around their long term savings plans and the speculation around changes only serves to have more people disengage from this critical area of their future financial plans. We echo calls from other commentators for cross party consensus on the position of long term savings so people can plan with a degree of certainty.

However, there is a raft of other changes including to rates of Capital Gains Tax and Inheritance tax on pensions that will have an impact on projections. The Envizage engine is designed to be flexible and configurable so we will be updating and publishing new configurations to reflect these changes. This will be published when the changes officially become law, ie when Royal Assent is given for the Finance Act, expected in the next couple of weeks.

Original article, 24 October 2024

With a week to go to the budget and a range of potential tax increase options being discussed, it is natural that many of us will be anxious about what this budget may mean to our financial future. At times like this, a financial plan can be invaluable in helping consumers visualise the impact of their choices and make informed decisions.

As an example, we examined how this budget might affect the financial plan for an affluent couple, David and Marta Jones. Here’s what we know about them.

- David is 55, earning £85,000 a year, and plans to retire at 60

- David has accumulated pension assets from various employers of £1m, whilst Marta has focused on building an ISA fund of £400,000 from the profits of her former business

- They plan to maintain their lifestyle after retirement, plus help out their children and use the extra free time to enjoy more holidays.

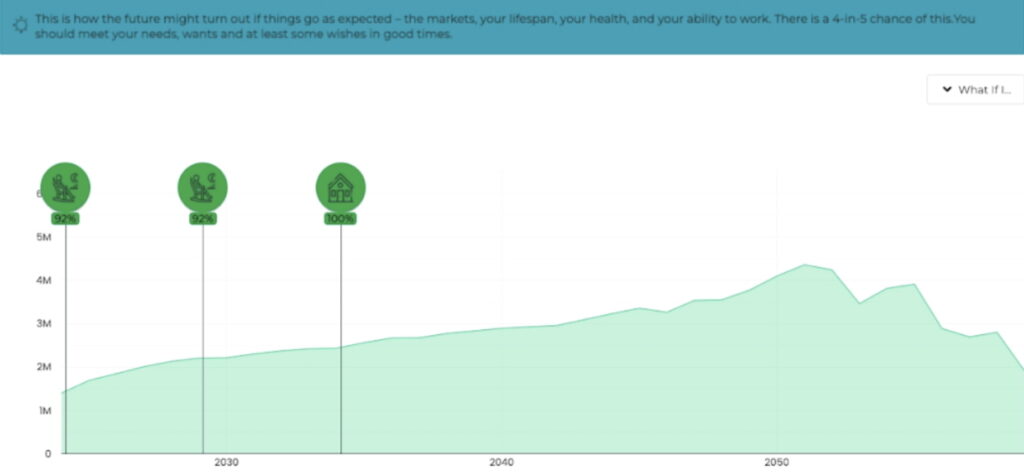

If we run this through the Envizage financial planning engine, we can see that the chance of the Jones achieving their lifetime plan is 92%. That is, taking into account both uncertainty in investment returns and uncertainty in life and health outcomes, only in less than 1 in 10 outcomes does the Jones family outlive their savings.

That’s a pretty solid plan. To get an even lower chance of outliving their savings, they would have to invest cautiously and protect against longevity. But that would impact their desired lifestyle spending.

Now let’s consider the impact of one of the possible tax changes – limiting pension tax free lump sums to £100,000. We chose this not because we think it may be likely (who knows what may or may not come out next week), but because for those it impacts, it’s emotive. And emotion seldom makes for good decisions.

The broad impact is that after retirement the Jones are now paying 40% tax on an additional £168,275 which was previously tax free. We model this by taking extra tax of £67,310 after retirement.

Rerunning their plan through the Envizage financial planning engine, we see that their chance of achieving their lifetime plan has now dropped to 90%. OK, no one wants to pay more tax, but it’s not a catastrophe.

We can also look at what happens if the Jones tried to get ahead of the budget by taking their £268,275 now and reinvesting outside of their pension. But because they have immediately lost the tax privileged investment roll up on this money, this actually decreases the chance of achieving their lifetime plan to 89%

Which is to say, in trying to get ahead of the change they have actually made the outcomes that they care about, in particular their retirement lifestyle, worse. They might pay less tax overall, but that comes at a cost to what they really care about.

This is just an example of what could happen for a hypothetical family, and was chosen to illustrate a point. Other individuals and families will have different changes to their plan for any given change in taxation or other factors which affect their plan. But the fact remains that having a dynamic financial plan can help you make better, more informed decisions.

At Envizage, we exist to help people achieve their desired future outcomes – whatever those outcomes may be for their personal situation. That’s why we want to make 2025 the year that we power financial services companies with the ambition to put a personal financial plan in everyone’s pocket.